Freeze Debt — an investigation

Another sponsored advert offering to help you ‘say good bye [sic] to debt’ on Instagram. I’ve had enough.

Freeze Debt. It’s marketed as a debt advice ‘app’. It doesn’t mention 87.2.9% write-offs or quote ‘little-known-about-government-debt-solution’ word risottos. But it does posit itself as a digital, easy-access gateway to multiple debt solutions, backed up by 1000+ rave reviews earning 4.1 out of 5 stars and 150,000 downloads.

The advert features a conservatively-dressed, older woman, subtly implying that this is an app that can be trusted, that there is sensible wisdom in downloading it for anyone struggling with debt. She is a more serious version of the glowing ladies who normally feature in IVA Lead Generator adverts — you know, the ones that look like they never lost a wink of sleep over debt in their lives – but the Freeze Debt persona is no less shallow for all her neutral tones.

I read some of the suspiciously formulaic reviews (‘I remember seeing this app on [a social media platform] and I wasn’t sure, but downloading it was the best thing I ever did ever’ etc]. I then downloaded the app. Was it the best thing I ever did? No, of course not.

The screengrab states that Freeze Debt is owned and operated by a company called ‘LOOCHI FINANCIAL LTD’. (According to Google, a ‘loochi’ is a deep-fried Indian yeast-free flatbread which gets puffed up during frying). I’ve a feeling ‘puff’ (in the advertising sense) is going to feature heavily in this review.

The small print also tells us that they are registered as a company in England and Wales and states:

Although our advice to you is free, we’ll be paid for introducing you or for the preparatory work we do.

If it walks like a duck, but identifies as an app, I think it’s still a duck. Is it the common showy, yellow-breasted lead-generator (pecunia argentum), or perhaps the equally widespread, but regulatorily more attractive, white-feathered debt-packagor (pecuniam capto)? (Compare this with the endangered debitum consilium).

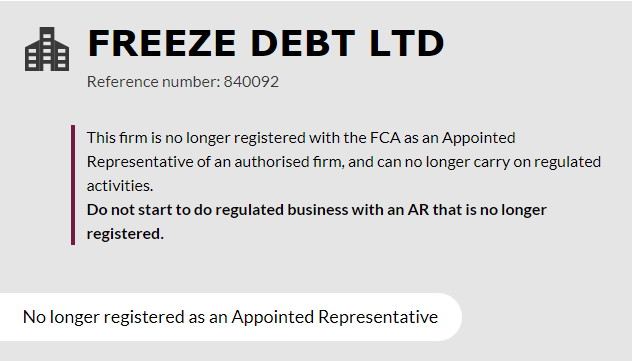

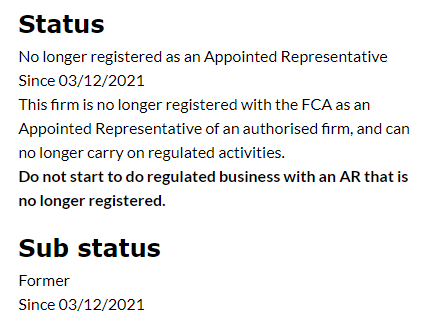

It’s marketed as a provider of debt advice, but this is a regulated activity, so they must be registered with the FCA. Let’s check.

Oh. That’s not a good start is it? Just so we’re clear, the FCA’s Consumer Credit Sourcebook (CONC) provides that ‘CONC applies to a firm with respect to carrying on credit-related regulated activities and connected activities, unless otherwise stated in, or in relation to, a rule.’

Some debt advisers are exempt, if they work for a local authority for instance, but complaints are then covered by the Local Government & Social Care Ombudsman, rather than the Financial Ombudsman Service.

Luckily, the FCA’s own register contains a direct link to Freeze Debt’s website (which is bonkers, if you think about it — here, have this link to a company we’ve just warned you not to do regulated business with). I wonder how many vulnerable people in debt go to the trouble of searching the FCA register before seeking advice from de-registered companies like this one?

The first thing you notice when landing on the Freeze Debt website is that they are keen to show you their awards. They even have a pop-up to remind you to spend some time admiring them. So I did. There are 8 in total, and I know it’s probably only a minor detail but it’s worth noting that the majority (5) are nominations and shortlistings, rather than awards per se.

Let’s have a quick look at one:

There is a link to the 2023 awards and photos of people having a good night out, but no information available about who the judges were in November 2021, when Freeze Debt won ‘Fintech Initiative of the Year’; we will have to assume they are all held in ‘high esteem’. The firm behind the awards is Barker Brooks Engaging Events and Trusted Media, (not exactly the Institute of Money Advisers) and they say this:

1.1.3 Our business. We hold business awards events for different industry bodies (Event(s)). For each Event we hold independently judged awards in various categories, as detailed on the website. For each entry made by your company there is, if applicable, a non-refundable fee (Entry Fee) which entitles your company to enter multiple categories, if relevant. We sell tickets for attendance at each Event (Tickets). For each company shortlisted for an award we offer the opportunity to purchase the Tickets.

So this is a sector within a sector isn’t it? Award ceremonies set up so that companies can purchase the veneer of legitimacy to showcase on their websites, possibly to replace the FCA registration they don’t got no more? Look at our awards! You can trust us, honest! Perhaps I’m too cynical, but I doubt it.

Moving away from the awards, the claims get bolder.

Freeze Debt is the UK’s leading debt advice and solutions app

Note the plural there — solutions — can’t just be IVAs then, can it? But how does an app – which clearly states within that it uses AI to determine the right solution – find itself becoming an approved intermediary for Debt Relief Orders?

By the way, I don’t believe for a second this app uses AI, but if it does, it’s shockingly on the blink.

And there’s that phrase ‘debt advice’ again. This is the UK’s leading (only?) AI debt advisor in app form. I’m sure that’s backed up by statistics somewhere and not just a heavily inflated piece of loochi.

…[O]ur debt advisors are experienced in finding solutions based on the individual circumstances of our users

They have debt advis-ors, and experienced ones at that apparently. I may have judged them too soon. Maybe they really are offering impartial, good quality debt advice?

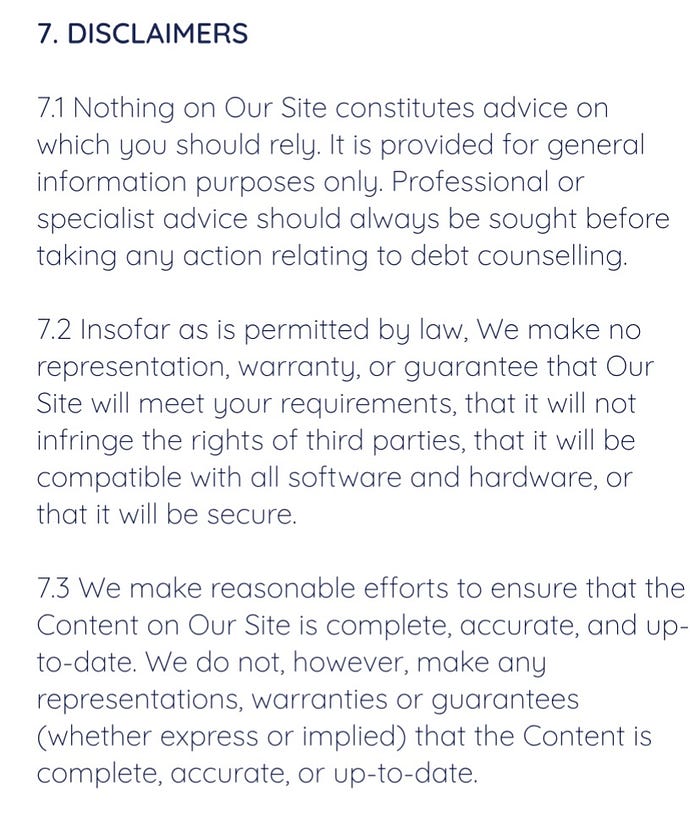

Wait, what? Read that again.

Nothing on Our Site constitutes advice on which you should rely.

But…the UK’s leading debt advice app? Experienced debt advisors? What do they do all day - puff up loochis? And do vulnerable people in debt read these disclaimers? Are they fully aware that this thing that markets itself as debt advice, isn’t?

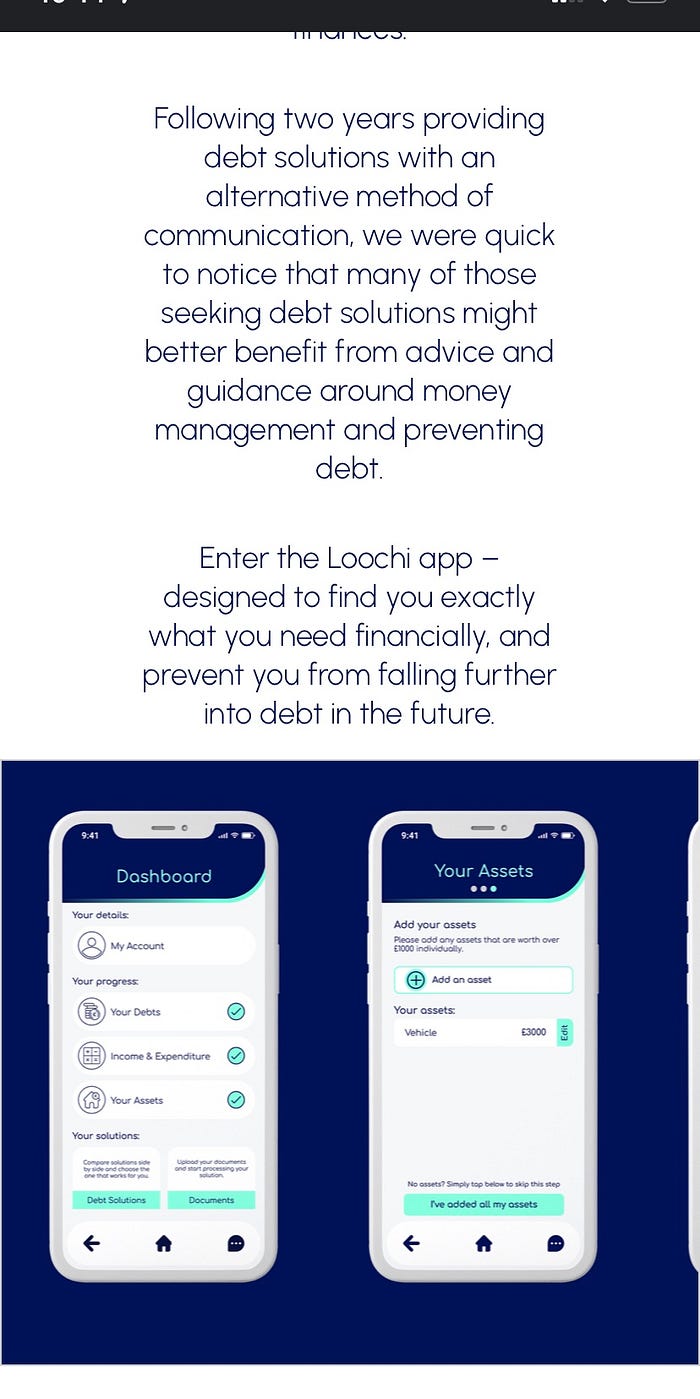

Their website explains the raison d’être for the ‘LOOCHI’ app. (Rebranded?)

But whatever you do, don’t rely on the advice…? I can’t mask my disappointment. According to the above, their debt advisors could not only help with debts now, but actively prevent you from falling further into debt in the future! How is this possible and how is this claim even legal, let alone sensible? Is Tom Cruise’s character in Minority Report behind this app ?— can they see when someone is going to fall into debt and send out a crack squad of advisors to divert people away from that health condition that prevents them from working, or that redundancy that they didn’t see coming? Amazing. I feel inferior. I can only advise on a client’s debt problems in the here and now…mind you, at least I stand by the advice I give. I call it ‘advice’ and confirm it in black and white.

There are two debt advisors listed on the Freeze Debt website, Qaasim and Andrea. I feel sorry for these two. They look quite young in the photos, and no doubt worked hard to gain all of that debt advice experience, to then suffer the indignity of their own employer issuing a disclaimer which cruelly suggests you can’t rely on a single a word out of their mouths? Shameful.

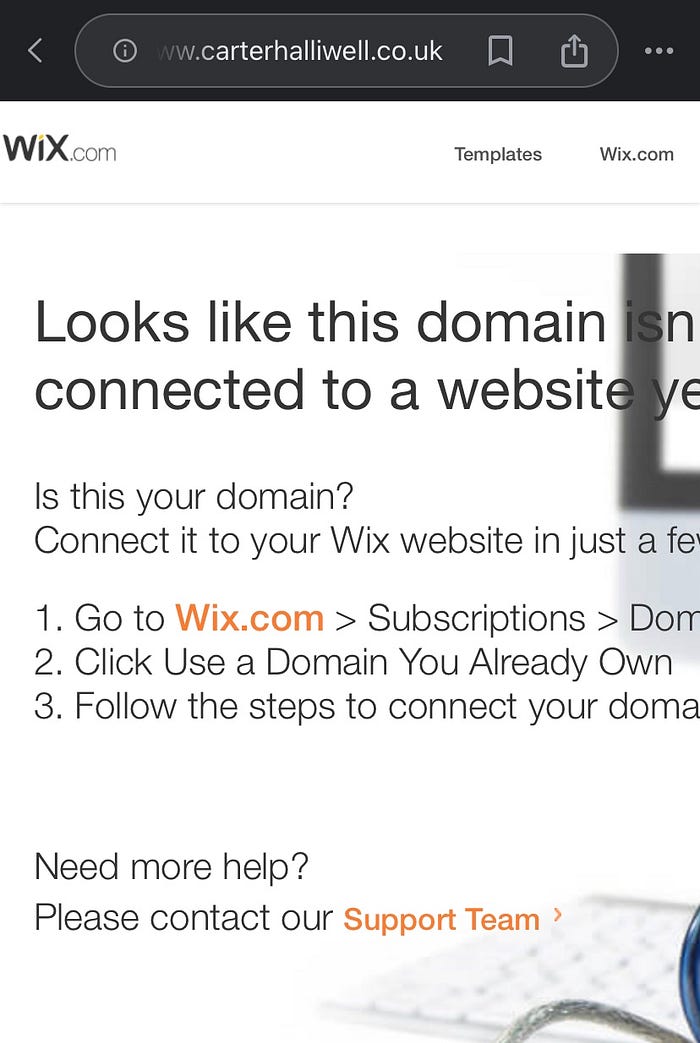

Freeze Debt also states it has a partnership with a company called Carter Halliwell — maybe their ‘experienced and talented team’ do debt advice?

Oh. They’re Insolvency Practitioners — and this is looking more and more like lead generation playing dress-up to be something else. I try the link inviting me to visit the website, but there isn’t one. A website, that is.

I google Carter Halliwell and there doesn’t seem to be a company website in existence; the first result is their Companies House listing.

Shocked to discover that the experienced and talented ‘team’ is in fact one-person;

- a former director of both Advice For Debt Ltd (a dormant company), and Howarth Bingham Corporate & Personal Recovery Limited, dissolved in 2016. Make of that what you will.

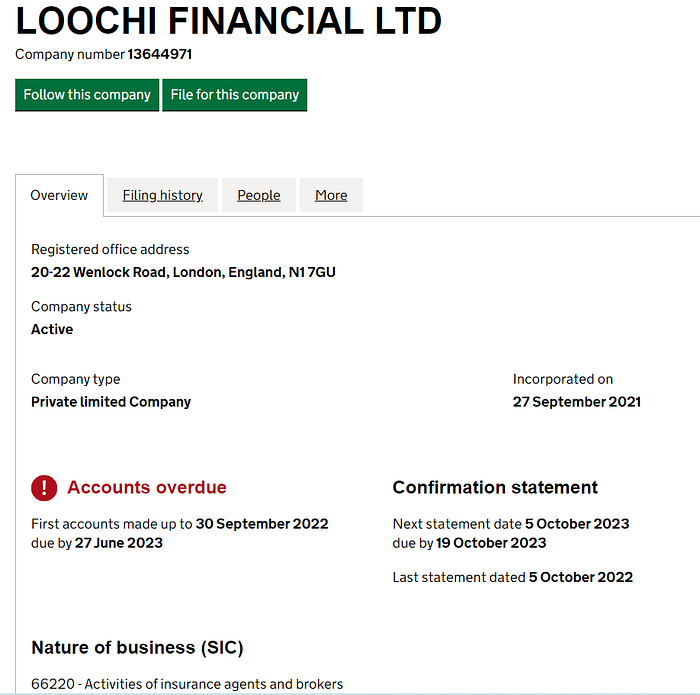

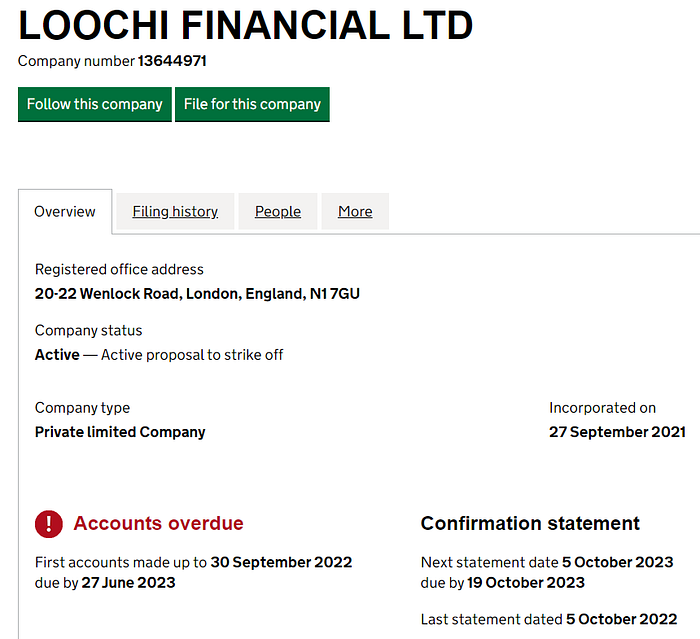

While I was on the Companies House website, I looked up Loochi Financial and took this screenshot a few days ago on 19/08/2023.

Again on 23/08/2023, spot the difference:

It doesn’t instil financial confidence, does it? Oh dear.

The Mystery Shop

Meet Ima Testin, a person in debt.

Ima duly completes the income, expenditure and debt sections with no assets, benefits-only income, £25 ‘disposable income’ and just less than £25k of debt. Ima ‘smashed it’, apparently.

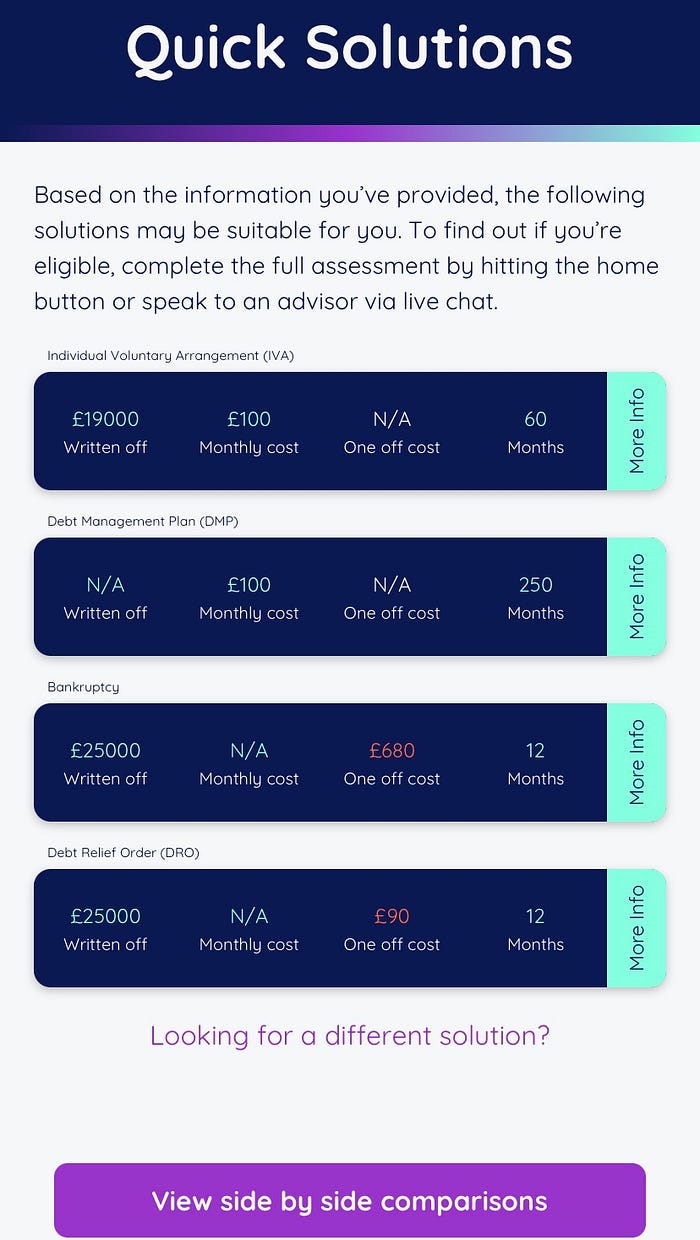

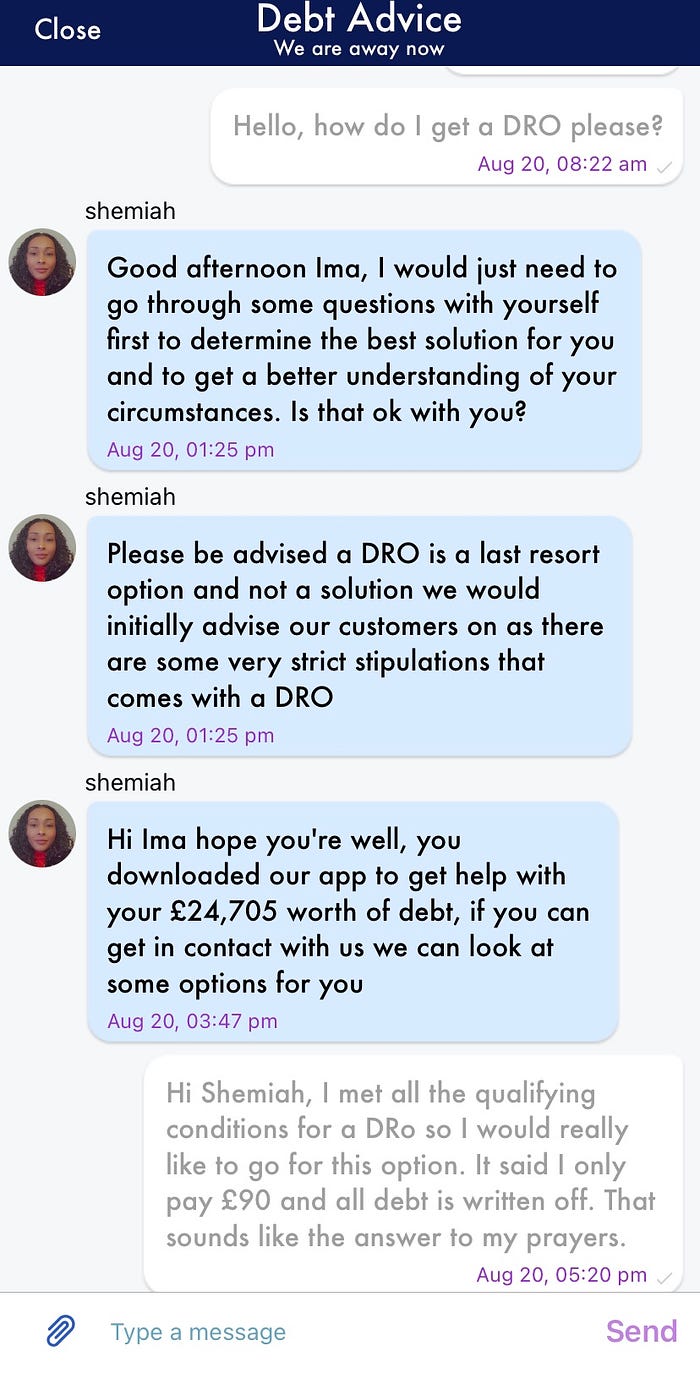

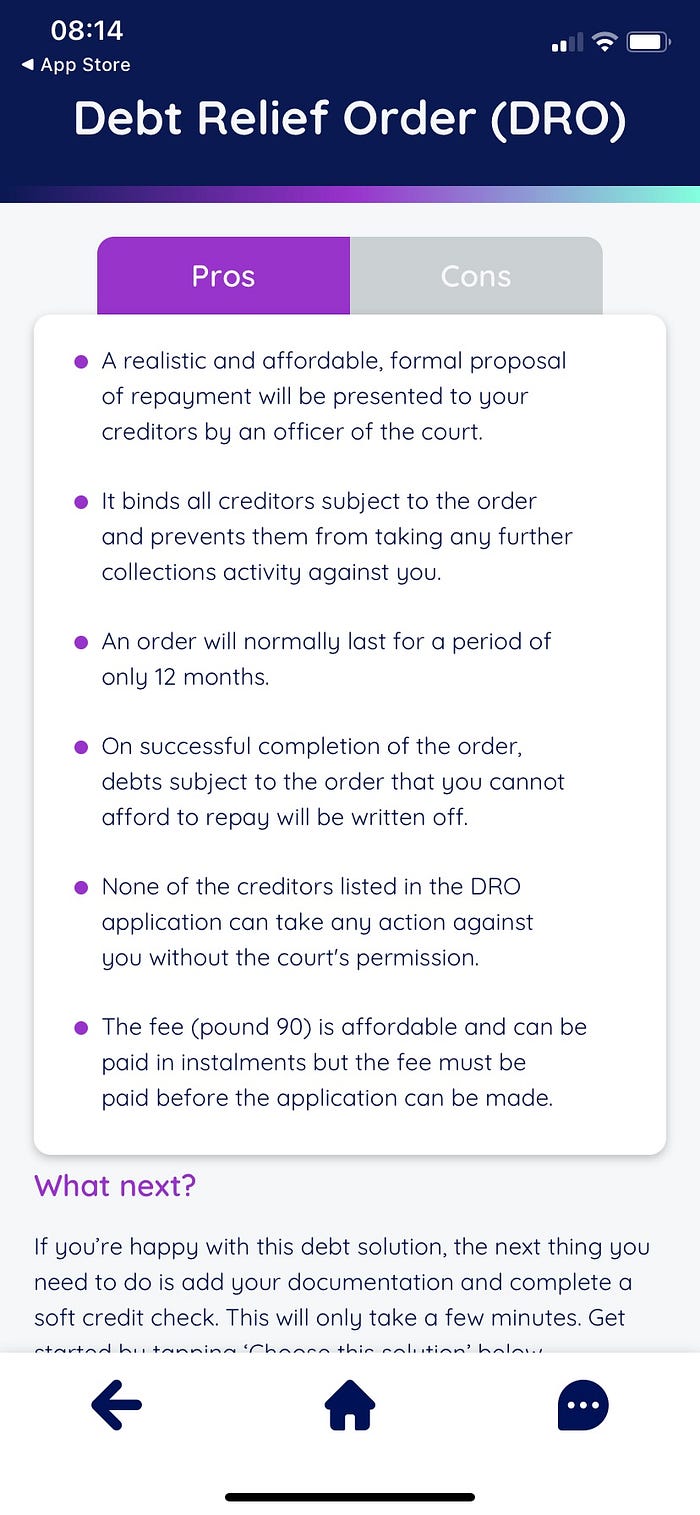

Prima facie, any debt adviser worth their CPD points is likely to be thinking about a Debt Relief Order on the information provided. But Freeze Debt believes this is the last option Ima should consider.

Their AI – clearly having a HAL 2001 moment – has determined that the first and second options Ima should be considering are, yes, you’ve guessed it, an IVA at £100 per month, or a Debt Management Plan at £100 per month. Of course, no-one in their right mind would pick the DMP over the IVA when faced with the information in the next screenshot below. So that’s an IVA then. And if I was a desperate person in debt, rather than a qualified debt adviser, I might not even give the DRO a second glance.

You have to wonder how Ima’s £25 per month of disposable income manifested such evidently unaffordable suggestions. I wonder if the ‘AI’ is simply programmed to suggest an IVA no matter what the income/outgoings? But that would be dreadfully misleading, wouldn’t it?

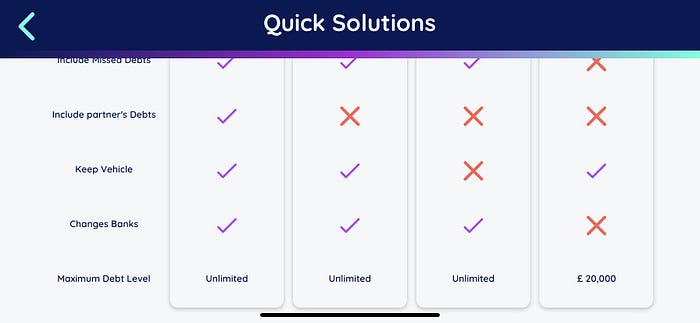

And the side by side comparisons also offer unreliable information. Look at the DRO maximum debt (far right). £20,000 hasn’t been the maximum for some time. I suppose the disclaimer about inaccuracy allows for these ‘slip-ups’?

Since registering, Ima has received text messages and an invite to connect with the advisors on WhatsApp, but as they have an in-app chat function, she sticks with that.

What follows appears to be an attempt to steer her away from a DRO, despite her assertion that, that’s the option she’s interested in.

A DRO a ‘last resort option’? Why? To see if Ima can be persuaded into a more lucrative IVA first? Any form of insolvency is ‘last resort’ really – it’s about reaching a point when debts can’t be paid back due to insufficient resources. Why do these companies treat IVAs as a less serious form of insolvency?

Maybe they don’t know exactly what a Debt Relief Order is, but it definitely isn’t this 👇

The above seems to be a cryptic mish-mash of IVA and DRO lore. What is Pound 90? Why not just say £90? (Come on Chat GPT! Do better!) The lack of accuracy in the above belies a laziness or reluctance to produce facts for a decent comparison of options. This means that debtors are expected to make the worst kind of decisions; those that are uninformed and based on misinformation.

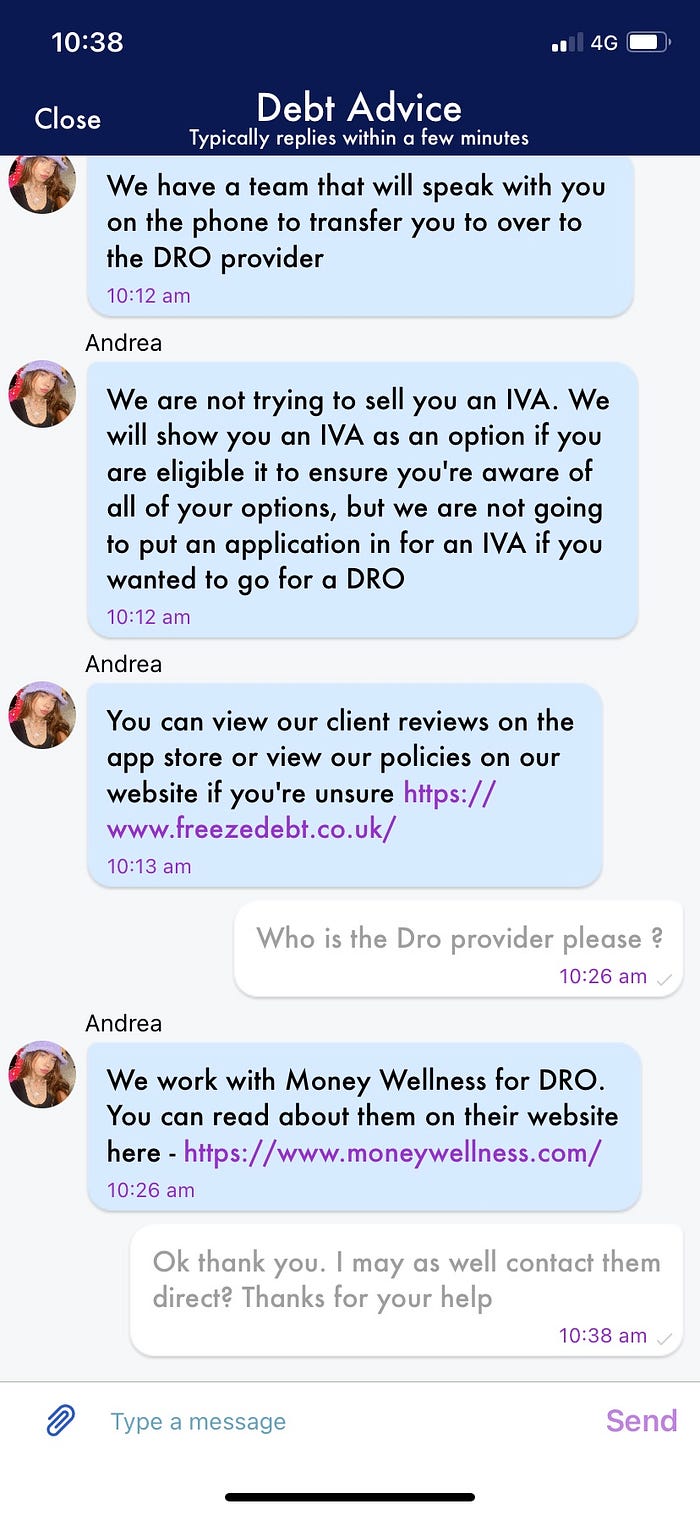

Ima persists with the next person on the message app. Do they do DROs or not? First they say they have a team, then they mention transferring Ima to a DRO provider, and when Ima expresses fear that they are trying to sell her an IVA, they add that they only show the IVA option if she’s eligible for it. But she’s clearly not eligible because she doesn’t have enough disposable income, so this is also not true.

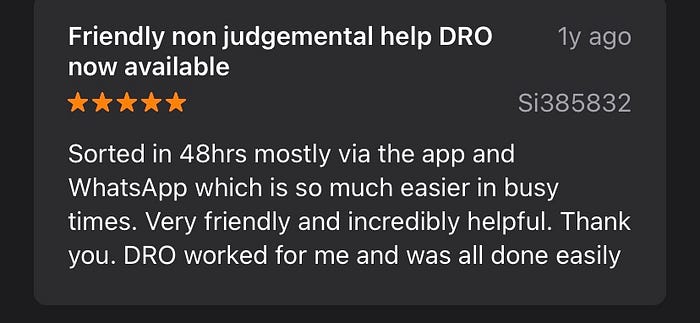

Now that Ima has established that they don’t do DROs themselves, despite one of their reviewers suggesting that Freeze Debt got their DRO approved in 48 hours (!), they say that they simply help to complete the form. This also can’t be true, because the actual online DRO application form is only accessible by approved intermediaries for the Insolvency Service.

Does this seem credible? Or did they write it themselves?

Ima’s next question is ‘who is providing the DRO?’

It’s Money Wellness, a trading style of Gregory Pennington Group. Money Wellness achieved something that many Insolvency Practitioners covet – the ability to process DROs – when they won a contract to provide debt advice from the Money and Pensions Service in late 2022, causing concern for not-for-profit debt advisers. DROs are strictly not profit-making. The ‘competent authority’ – in my case, the IMA – receives £10 of the £90 DRO fee for each DRO, essentially because debt advisers do most of the administrative work. There’s no ‘big money’ to be made though.

Gregory Pennington is at least FCA registered though, so it’s even more worrying that Money Wellness say this about DROs on their website:

This is not true. Significant improvements in finances do need to be reported to the DRO Unit, but decisions are made on a case by case basis and take into account multiple factors, such as how significant the increase in income is, the size of the moratorium debt etc. A debtor moving from benefit-only income to earnings should not fear having their DRO automatically cancelled. The Insolvency Service does not seek to punish people getting into work, because this could dissuade people to seek out a debt solution in the first place. Disappointing.

And now I have another question, not yet answered. Does Money Wellness pay Freeze Debt for DRO leads? If so, why?

Debt advice is obviously a highly lucrative market for some and this is nothing new. The problem is that people in unmanageable debt don’t have lots of money to play with, so they can’t afford to pay for debt advice. Ultimately, the creditor pays, and as I’ve described before in other blogs, the secondary debt market can still do very nicely out of this arrangement, as can the Insolvency Practitioners, lead generators, debt packagers etc.

The MaPS contract being awarded to a commercial, profit-making company was a chilling moment for not-for-profit debt advice. Many debt advisers, including me, saw it as a juncture at which the polluter got a foot in the door for a profit-driven sector perhaps seeking to eradicate NFP debt advice altogether. But where will all the failed IVA customers and vulnerable people who, for a variety of reasons, need in-person advice then go for help?

And it’s those people in debt that I am trying to speak up for. Those that are genuinely struggling to make ends meet and being coerced into unsuitable options which make their situations worse. When people contact me privately, on social media platforms, and tell me they are having ‘dark thoughts’ because they are trapped in IVAs they can’t afford, then I have to speak out…because there’s this (seen on Twitter):

I worried about publishing this – I don’t have a huge platform to speak from but it’s not insignificant either. The CEOs of these companies won’t like negative reviews, but this is truthful. People struggling with debt, brave enough to ask for help deserve absolute truth and transparency when they seek out possibly life-changing advice.

I make no apology for it. I want this sector and the regulators to do better. Do more to protect people whose unmanageable debt is making their lives a misery. And to the CEOs, there must be better ways to get rich quick? Have you considered crypto?